When planning ahead, it’s important to acknowledge the events of the last financial year, as well as the climate in which businesses are currently operating. The impacts of the ongoing pandemic, extreme weather events, continued supply chain disruptions, the invasion of Ukraine and subsequent inflation pressures, plus a rising interest rate environment are all significant challenges that impact operations and decision-making in one way or another.

So, amid this uncertainty, how should you plan for the year ahead?

During the new financial year, practice owners will hopefully be able to leverage new opportunities and say yes to a lot more exciting possibility. But as the adage goes, “Before anything else, preparation is the key to success”.

the top five most important global risks for businesses are cyber incidents, business interruption, natural catastrophes, pandemic outbreaks, and changes in legislation and regulation

As another financial year comes to a close, it’s a great time to reflect on your business strategy and decide how you can get your financials and tax position in better shape over the next 12 months. After all, circumstances change and there’s always room for improvement.

With continued uncertainty about exactly how the fiscal year will play out, understanding the headline risks will allow you to manage what you can control. According to the Allianz Risk Barometer 2022, the top five most important global risks for businesses are cyber incidents, business interruption, natural catastrophes, pandemic outbreaks, and changes in legislation and regulation.

Fortunately, at an Australian level, the local economy has continued to prove resilient and has outperformed expectations. Many lessons on adapting, flexibility and preparedness have been implemented by small to medium-sized businesses since the global pandemic began. And the government remains focused on its economic and fiscal recovery strategy, aiming to help small businesses do what they do best as the “engine room of our economy”.

In the 2022-23 Federal Budget, delivered on 29 March, small businesses were offered tax relief plus bonus tax deductions on technology and training to help companies embrace the digital revolution, as well as improve cash flows.

But the challenge everyone’s watching is how we shift from the low-interest rate inertia. The Reserve Bank of Australia is gearing up to raise the official cash rate for the first time in 11 years. Experts believe this will occur before June, with expectations for interest rates to be around 1.5% by the end of 2022, at the time of writing.

Amid this ever-evolving context, here’s our checklist covering the key areas that business owners can control, and therefore should assess, as we welcome the 2022-23 financial year.

By proactively planning and implementing some of the recommendations appropriate for your business, you may find ways to save money, achieve better cash flow, and reduce your overall tax bill to enable you to continue to achieve growth and success, while doing meaningful work.

WHAT SHOULD YOU BE REVIEWING NOW?

Evaluate Your Cash Flow

Assessing your cash position is paramount to your practice’s day-to-day running and future success. An accountant is a valuable advisor who can help you make informed financial decisions, including superannuation, as well as maximising your tax deductions and reducing the tax you pay. They can help you understand your tax obligations better, as well as guide your future tax plan, and map out your tax instalments to avoid being hit with a huge tax bill.

Take the time to ask yourself or go through with your accountant:

- How did your income or earnings go for the year?,

- How does that compare to the previous year in terms of unexpected tax liabilities?, and

- What can you do to minimise that liability?

Pre-empt Your Expenses and Purchases It’s always a mad rush to the end of financial year (EOFY), with decisions to finally buy business assets often made last minute. But what if you could lessen the EOFY strain for next time?

With a new financial year comes an opportunity for business owners to review their strategy and growth plans, and from there, build out a 12-month budget. This allows you to have a good overview, particularly for surprise expenses or unplanned purchases, in addition to being able to see how you are tracking when needed, typically each month or quarter.

You could also look at ways to reduce the burden of expenses:

- Negotiate with service providers, suppliers and vendors for a more competitive price and/or repayment terms,

- Buy in bulk to save over the long term,

- Be in a positive cashflow position to be able to purchase during seasonal promotions or sale periods and benefit from substantial savings, and

- Think beyond cash and consider financing options.

Typically, there are significant tax benefits that come with business use purchases. If you are considering purchasing assets for your practice, such as new equipment, upgrading your practice fit-out or even a new car for work purposes, presenting this information to your accountant as early as possible will give you an advantage when it comes to planning out your tax bill.

Temporary full expensing was extended to 30 June 2023 and then it stops. You should consider whether making capital purchases in this financial year, and the next, is more optimal i.e. spread the deduction over two tax periods rather than making a mad dash this time next year. Always check in with your accountant about your specific circumstances in relation to this incentive.

As part of your purchase decision-making, it’s also crucial to ask whether the purchases you’re planning to make will future-proof your business. Are you continuing to invest in technology?

The benefits of doing so include improving security, efficiency, and productivity gains, having a competitive edge, better interaction with your patients, and enabling remote access. When combined, these outcomes can contribute to an increase in profit, so remember to keep the bigger picture in mind.

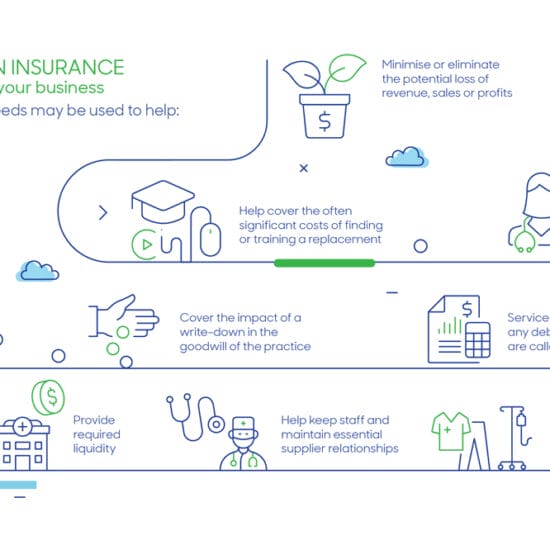

Consider Your Financing Options

You may find that you need to boost your cash flow or increase it. Often, it can feel like small and medium businesses are doing it all on their own, but the evolving lending market means there are now alternatives. This means you could be one step closer to finally purchasing that new piece of equipment you’ve been saving up for. And your business may not have to bear the full cost, or can perhaps leverage lending arrangements like Buy Now Pay Later.

A few financing avenues include:

Buy Now Pay Later arrangements

These aren’t just for patients, but are available for business equipment, fit-out and vehicle purchases where liquidity, tax deductions and the time to optimise equipment use are among the many benefits that can be unlocked for your practice.

Business loans

These can cover you for practice purchases, commercial property, goodwill loans, equipment and fit-out finance. Talk to a specialist medical lender to discuss the types of financing available to you.

Private investors or financiers

Understanding the pros and cons of this alternative private funding source is crucial to its success.

Government grants

The government’s business grants and programs often offer funds, assistance or rebates to enable expansion, commercialisation, and research and development.

Industry grants

Certain companies and institutions have designed grants to help businesses during various phases of their business life cycle or during tough times. Credabl’s Helping Hand Grants is one such grant that will return this year to support small and medium-sized businesses in the profession.

Review your loans

The competitive nature of lenders means you can no longer afford to “set and forget”. Changing rates, fees and charges, plus terms for the finance could leave you either better or worse off. This is why a financial health check and sticking to regular reviews are necessary.

Refinancing your loans can help you get some cash flow back – and this includes any residential loan obligations, as you may require an overall debt restructuring, potentially consolidating all debts to a single lender. Doing so could mean lower rates, while also replacing the need to manage many separate repayments into one monthly repayment, for example.

Changing to a specialist lender who understands the ins and outs of your profession will also come in handy for when you need to access cash, if your personal or professional circumstances have changed, or if you foresee any changes to your income structure.

ENGAGE THE RIGHT EXPERTS AND ADVISORS

When dealing with a lender, it’s imperative that you deal with experts who know your profession and speak your language. From accountants, lawyers, equipment vendors, builders, and even practice management leaders, through to finance specialists, they need to know the ins and outs and can help you along your journey.

Remember, preparing a stable and growth-centric strategy for your finances will mean you’ll be in a better position to take advantage of fiscal year peak periods and exciting opportunities. It will also help keep the business going during slower seasons or more challenging periods.

Stafford Hamilton is Chief Executive Officer and co-founder of Credabl – medical finance specialists with a deep understanding of the optometry and ophthalmology professions. The team at Credabl can support your plans to achieve your new financial year ambitions. Visit: credabl.com.au or call (AUS) 1300 273 322.

This article is a guide only and does not constitute any recommendation on behalf of Credabl Pty Ltd (ACN 615 968 100) or any of its related bodies corporate (Credabl). The information in this article is general in nature and we have not considered your personal objectives or financial circumstances or needs when preparing it. Before acting on this information you should consider if it is suitable for your personal circumstances. Credabl is not offering financial, tax or legal advice. You should obtain independent financial, tax and legal advice as appropriate.