Purchasing property through your self-managed superannuation fund (SMSF) could prove a good avenue for diversifying your investment strategy.

In a world of uncertainty, planning for your retirement has never been trickier. With changing governments, the next wave of the pandemic, consecutive Reserve Bank of Australia interest rate rises, rising and falling home values, and an unpredictable state of affairs on the world stage, there are many external factors outside of our control. However, this shouldn’t deter you from planning for your retirement. With the correct guidance and advice, investing through a SMSF can still be a financially viable structure to help grow your wealth portfolio in a tax effective manner.

With the right guidance and advice, investing through your SMSF can be one of the most tax-effective and financially rewarding wealth creation strategies

Having said that, financing investments through an SMSF has gotten more complex over the years. Most of the banks (including the Big 4) have departed the market as recently as 2018, leaving only a handful of second-tier lenders willing to lend to an SMSF.

WHAT TO KNOW ABOUT SMSF

An SMSF is your own superannuation fund, that you personally manage and have control over. It is set up for the purpose of providing benefits for its members upon their retirement. While there are no requirements regarding minimum balances to set up an SMSF, there is a general consensus that one should have at least AU$500,000 to make it viable.

Once your fund has been set up, you can roll over your existing superannuation benefits into your SMSF and start making your personal contributions directly to the fund. There are limits to the amount of contributions you can make yearly. These are known as the ‘contribution caps’. If you exceed the limit, it may cost you additional tax. You’ll need to verify the amounts with your accountant and/or financial advisor.

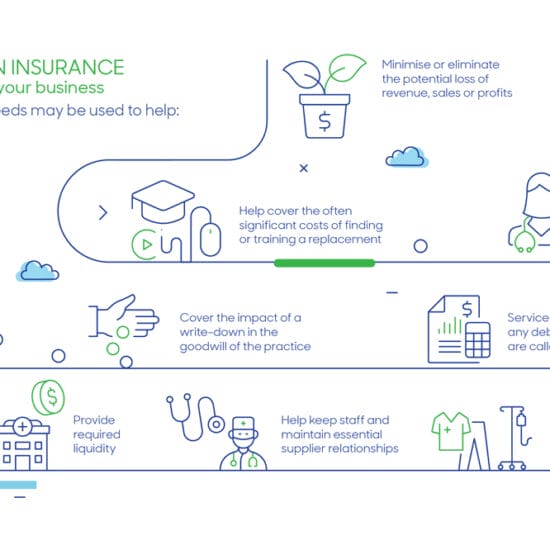

Certain insurances can also be funded through an SMSF.

It is strongly advised that you obtain financial advice from a licenced financial adviser prior to setting up your own SMSF, as getting the structure, compliance and legal matters correct is critical.

It’s also important to weigh up the pros and cons of using a SMSF to build wealth. On the positive side, you will have greater control over your investments, gain tax benefits as income earned is taxed at a lower rate of 15% (down to 0% upon retirement), have asset protection, and often greater flexibility regarding choice of investments. This extends to term deposits, residential or commercial Australian property (including off-the-plan purchases), Australian and international shares, managed funds, bonds, and cryptocurrency.

However, using an SMSF can be more costly, requiring legal and financial advice, asset valuations and insurances. It can also be more onerous, due to ongoing compliance obligations, including annual audits, financial statements, and tax returns. As well as this, when moving to an SMSF, there is the risk of losing the current insurances you hold in an industry or retail super fund, and new policies in the SMSF may mean higher costs.

Importantly, you need to be aware that all members are responsible for all decisions made by the fund and must comply with the super and tax law.

KEY RULES FOR BORROWING THROUGH YOUR SMSF

SMSF is a complex field, with key requirements to consider when borrowing.

All investments must be on a commercial ‘arm’s length’ basis (i.e. market value). This includes the purchase price of investments, as well as the income (e.g. rental on properties).

Borrowing through SMSF is deemed to be a ‘Limited Recourse Borrowing Arrangement’ (LRBA), which means if the SMSF defaults on its loan(s), the bank is unable to pursue other assets in the fund to recoup lost funds, but may seek recovery from the individuals. This, and other complexities of the legislation around LRBAs are partly responsible for why banks perceive SMSFs to be higher risk. Therefore, the Loan to Value Ratios (LVRs) that the banks typically look to lend on sit in the 70–80% range (meaning you need to come up with 20–30% deposit). This can be compared to the more favourable 90% LVR some lenders will allow you for your owner-occupied residential home, by virtue of your vocation as an optometrist/ophthalmologist.

It’s also important to note that you cannot borrow to fund construction or use equity in existing assets as security for borrowing. And, if you borrow to buy a new asset and it goes up in value, the equity/loan amount repaid can’t be used as security for borrowing.

As well as this, some lenders require evidence of independent financial advice regarding your SMSF. Should you need guidance/advice in this area, Optometry Finance Australia has an association with an SMSF accounting specialist and adviser you can get in touch with.

BORROWING FOR RESIDENTIAL PROPERTY THROUGH SMSF

As touched on above, borrowing through your SMSF can be more challenging than traditional borrowing for residential property, due to the risk that the banks associate with the security (including the lack of recourse). Additionally, you can’t buy the residential property from fund members or other related parties, and you can’t rent the residential property to a related party, even if it is on a commercial arrangement.

Some of the differences we see when borrowing through an SMSF (as opposed to outside SMSF) include:

- Interest rates can be higher by 2 –2.5% (the higher the risk, the higher the rate),

- LVRs to a maximum of 80% (more deposit reduces the bank’s exposure),

- You can’t borrow to acquire vacant land,

- May be used to fund houses, units, townhouses and apartments,

- SMSF loans are often harder to service than normal residential loans (due to higher LVRs, and only 80% of rental income being used in the servicing calculations),

- A personal guarantee is required by the SMSF Trustee, and

- Most financiers require you to get independent financial advice.

BORROWING FOR COMMERCIAL PROPERTY THROUGH SMSF

If you have been leasing someone else’s property to operate your own practice for a number of years, it may be time to consider investing in your own commercial property. One of the advantages of having the property in your SMSF is the tax benefit, with the rental income attracting only a 15% tax rate.

Contrary to residential properties, a commercial property can be acquired from, and rented to fund members and related parties, provided it is done at arm’s length.

Where you already own your practice premises in an entity that isn’t an SMSF, it may also be appropriate to consider a restructure, where there could be some capital gains tax and / or stamp duty concessions available to restructure your arrangements to achieve a superior longerterm outcome.

Investing in, and the financing of, your commercial property through your SMSF also has some further nuances that you need to consider.

For example, the servicing (repayment) calculation of the monthly mortgage commitment can be met through a combination of rental income (usually limited to 80%), as well as other investment income and your own (member) contributions. Why pay someone else’s rent to run your practice, when you can be paying off your commercial mortgage with a long-term view to owning the premises yourself?

Commercial properties are often deemed by the banks to carry more risk than residential properties, as they are often harder to dispose of in the (unlikely) event of foreclosure by the bank. They’re also a little harder to value. As a result of this, the banks look to ‘mitigate’ this perceived risk by lending to a lower LVR (often 70–80%), requiring more up-front contribution (deposit) by the SMSF.

Commercial loan terms of up to 30 years Principal and Interest (P&I) are generally available, with up to five years initial Interest Only loans (which then revert to P&I), and the property may be valued on a vacant possession and alternative use basis.

Generally, independent financial advice is required, however not by all lenders. Refinancing within your SMSF is possible, often with minimal requirements.

REFINANCING RESIDENTIAL PROPERTY IN SMSF

If you haven’t done so in the last four to six years, now is probably a good time to contact a broker that specialises in financing through SMSF to help revisit your current lender and mortgage, as many of the banks that were financing in SMSF back then have left the market. It’s possible the variable rates you are currently on are excessively high.

Depending on the lender, refinancing can be a fairly painless (yet financially worthwhile) exercise, with some lenders only requiring the last 12 months SMSF loan statements (ensuring good payment conduct), a completed servicing calculator, and proof of 12 months gross rental income (which must cover the proposed loan repayments).

SUMMARY

There are lots of rules and complexities when it comes to investing through a SMSF. But don’t let this frighten you off. With the right guidance and advice, investing through your SMSF can be one of the most tax-effective and financially rewarding wealth creation strategies.

You may wish to speak to a finance broker who will have access to the various financial institutions that fund for SMSF purchases. They can help guide you through the specific requirements lenders have, and help get you pre-approved. With the pre-approval in hand, you can often negotiate on price, as you present from a position of strength where finance is no longer an obstacle for you.

Paul McKinley is the Managing Director and resident Chartered Accountant of Optometry Finance Australia, an independent finance broker that works with optometrists Australia-wide. With over 30 years of relevant commercial experience in the finance, automotive and accounting industries, Mr McKinley specialises in commercial funding with a strong focus on personalised client service and retention.

Visit: optometryfinance.com.au.

The information contained in this article is for general information purposes only and should not be construed as investment or financial advice. Any decisions regarding commitments of a financial nature should only be made after appropriate advice from a qualified and registered financial or investment adviser.